Bank Of Canada cuts rates by quarter percent

Sep 4 2024 ,The Bank of Canada’s decision to cut the interest rate by a quarter percentage point reflects its aim to address economic challenges, including slower growth and rising concerns about inflation. By reducing borrowing costs, the central bank hopes to encourage consumer spending and investment, providing a much-needed boost to the economy. This move is particularly significant given the sluggish housing market, which has faced headwinds due to higher borrowing costs and affordability concerns.

| Date | Reference | Previous | After Meeting | CPI |

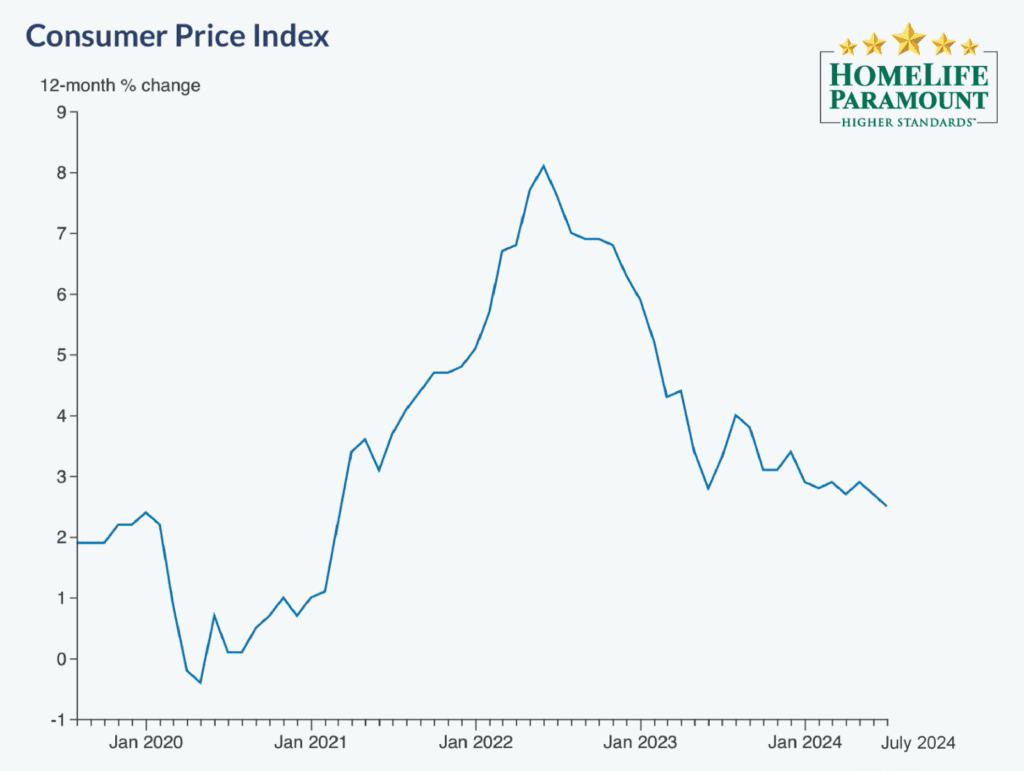

| 10th April 2024 | BoC interest Rate | 5% | 5% | 2.7 |

| 5th June 2024 | BoC interest Rate | 5% | 4.75% | 2.7 |

| 24th July 2024 | BoC interest Rate | 4.75% | 4.5% | 2.5 |

| 4th Sep 2024 | BoC interest Rate | 4.5% | 4.25% | 2.5 |

The rate cut is expected to have a positive impact on the housing market, especially as we move into the fall and winter months. Lower interest rates generally make mortgages more affordable, which could stimulate demand among potential homebuyers who have been hesitant due to higher rates. This increased demand might help stabilize home prices and improve market conditions, offering a more favorable environment for both buyers and sellers. At Homelife Paramount, we ensure you are kept up-to-date with these crucial industry changes, helping you make informed decisions in a dynamic market.

In its September 2024 meeting, the Bank of Canada (BoC) cut its key interest rate by 25 basis points to 4.25%, following a similar 25 basis point reduction in June and July. This move, anticipated by some in the market, continues the easing from the terminal rate of 5%, which had been maintained for 10 months. The BoC’s Governing Council highlighted that the excess supply in the Canadian economy has recently helped reduce inflation, justifying a looser monetary policy. Additionally, the Canadian labor market is showing signs of slowing down. The central bank noted that lower interest rates, coupled with indicators of excess supply, could help reduce costs for mortgages and shelter, which have been major drivers of inflation. The Governing Council expects CPI inflation to decline in the second half of the year, partly due to base effects from gasoline prices, and to stabilize around 2% in 2025.

Impact on Mortgage Savings:

A 25 basis point rate cut results in only a modest reduction in monthly mortgage payments. For example, a borrower with a $600,000 mortgage, a 25-year amortization, and a 4.5% interest rate would save about $88 per month if the rate dropped to 4.25%.

Impact on Lines of Credit and Credit Cards:

Lines of credit are usually linked to the bank’s prime rates, so borrowers might experience some savings if banks reduce their prime rates following the BoC’s rate cut. However, credit card rates tend to be more fixed, so consumers should not expect significant changes there.

Impact on Savings Accounts and Guaranteed Investment Certificates (GICs):

Savings accounts and GICs had been offering higher returns as interest rates rose, but these could decline if prime rates decrease in line with the Bank of Canada’s actions. GIC rates have already begun trending down in anticipation of further rate cuts, although some smaller financial institutions are maintaining higher rates to attract customers.